Part III — Core Hunting Techniques · 7 min read

Covered Call and Cash-Secured Put — The Pack’s Income

"Slow income, steady income. The pack feeds on discipline, not heroics."

The "Risk-Free Income" Lie — Say It First

The truth: covered calls and cash-secured puts shift some directional risk into premium collection. They do not eliminate risk. They reshape it.

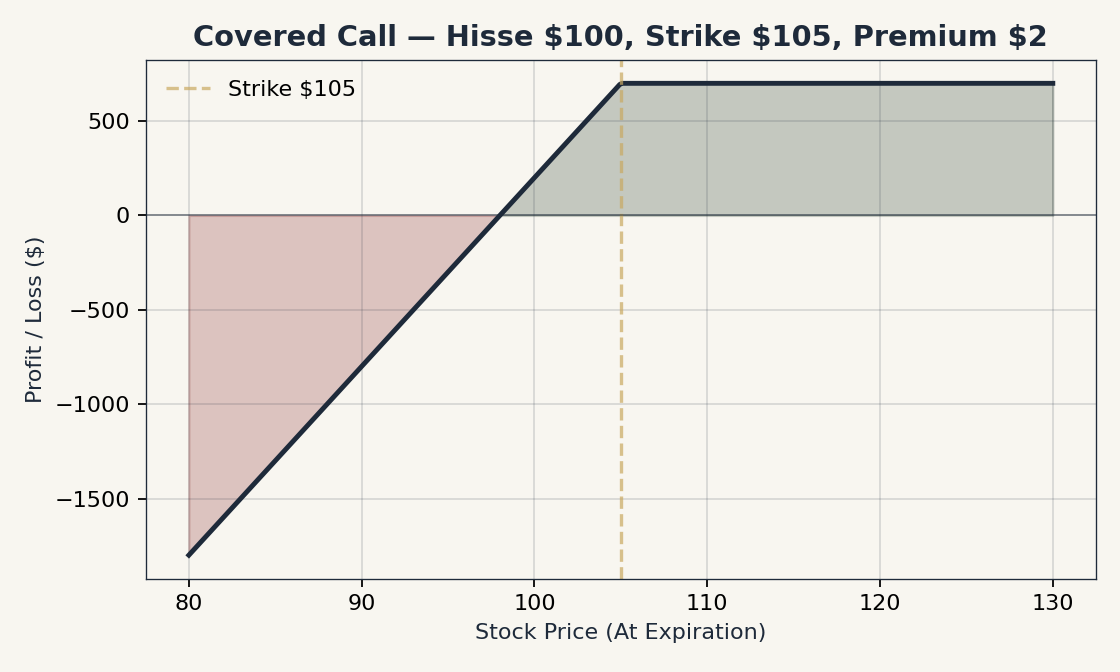

Covered Call (CC) — The Pack’s Monthly Tip

Mechanic

-

You own 100 shares of an underlying (for each contract).

-

You sell an OTM call against those shares.

-

If the stock stays below the strike, the call expires worthless, you keep the premium.

-

If the stock rises above the strike, your shares are called away (sold to the call buyer at the strike). You miss any further upside.

Strike Selection

-

Delta 0.20-0.30 → ~70-80% chance of staying OTM. Modest premium.

-

Closer-to-the-money strikes → richer premium but higher assignment risk.

-

Further OTM → minimal premium, less compelling.

The "right" delta depends on your view:

-

Pure income (you want to keep the shares): delta 0.15-0.20.

-

Income + willing to part with shares above target: delta 0.25-0.35.

-

Aggressive sell-the-rip: delta 0.40+ on overextended names.

Cash-Secured Put (CSP) — The Patient Hunter

Mechanic

-

You have cash equal to (strike × 100) set aside.

-

You sell an OTM put on a stock you would be happy to own at that strike.

-

If the stock stays above the strike, the put expires worthless, you keep the premium.

-

If the stock falls below the strike, the put is assigned — you must buy the stock at the strike.

|

A cash-secured put is a strategy to "buy a stock you already wanted, paid to wait." If you do not want the stock at the strike, you have no business selling the put — assignment will hand you a stock you never wanted, at a price the market has already deemed too high. |

The Wheel

The Wheel strategy is the continuous loop of CSPs and CCs:

-

Identify a stock you want to own long-term.

-

Sell a CSP. If it expires worthless, collect premium and repeat.

-

If assigned, you now own the stock.

-

Sell a CC on the stock. If it expires worthless, collect premium and repeat.

-

If called away, you no longer own the stock. Return to step 2.

The Wheel works if and only if you would be happy to hold the underlying through a drawdown. If you would panic-sell at -20%, the Wheel is the wrong strategy.

Greeks on These Strategies

| Greek | Covered Call | Cash-Secured Put |

|---|---|---|

Delta |

Long stock +1.0, short call −0.30 → net ~+0.7 (still long-biased) |

Short put → +0.30 (long-biased) |

Theta |

+ (in your favor — premium decays) |

+ (in your favor) |

Vega |

− (IV decay helps short option) |

− (IV decay helps short option) |

Gamma |

− (negative gamma intensifies near expiry) |

− (negative gamma intensifies near expiry) |

Both strategies are short volatility and short gamma. They make money in calm markets and lose money in violent moves — particularly violent moves against you.

Management

-

50% profit: A short option you sold at $1.00 is now $0.50. Close it. Why? Theta has decayed nearly half the extrinsic; the remaining $0.50 will take longer and longer to harvest, with rising gamma. Better to close and redeploy.

-

Loss management: A 100-200% loss (premium has doubled or tripled) is your typical "manage or cut" threshold. Roll out in time, roll out and down (for CSPs), or accept the loss.

-

21 DTE: Per the 21-DTE convention (see Chapter 10), short positions are typically closed or rolled at 21 days regardless of P&L, to avoid the gamma cliff.

-

Ex-dividend on CCs: monitor closely. If extrinsic value falls below upcoming dividend, your short call is a candidate for early exercise (Chapter 9).

-

Earnings: short premium into earnings is a popular play (you benefit from IV crush), but the directional risk is binary. Reserve this for advanced traders.

Common Mistakes

-

Selling CSPs on stocks you don’t want to own: when assigned, you hold a stock you hate. The premium does not compensate.

-

CCs too close to the money: assignment is frequent, upside is sacrificed cheaply.

-

Treating the Wheel as risk-free: A 30% drawdown on the stock is a 30% drawdown on the position, premium notwithstanding.

-

CCs going into ex-dividend: early assignment costs you the dividend.

-

Five CSPs in the same sector: in a sector sell-off, all five assign at once. You have effectively concentrated your account.

Tax Note

Brief and entirely informational, not advice (see Disclaimer):

-

Premium received on a short option that expires worthless is generally short-term capital gain (US individual taxpayer perspective).

-

Assignment on a short call (covered call) becomes part of the stock-sale price for cost-basis purposes.

-

Assignment on a short put (CSP) reduces the cost basis of the assigned shares.

-

Consult a tax professional. The above is a sketch, not gospel; rules differ by jurisdiction and entity.