Part III — Core Hunting Techniques · 5 min read

Protective Put and Collar — Armor

"Armor that has never seen battle is foolish. Armor that fits poorly is worse — it is dead weight."

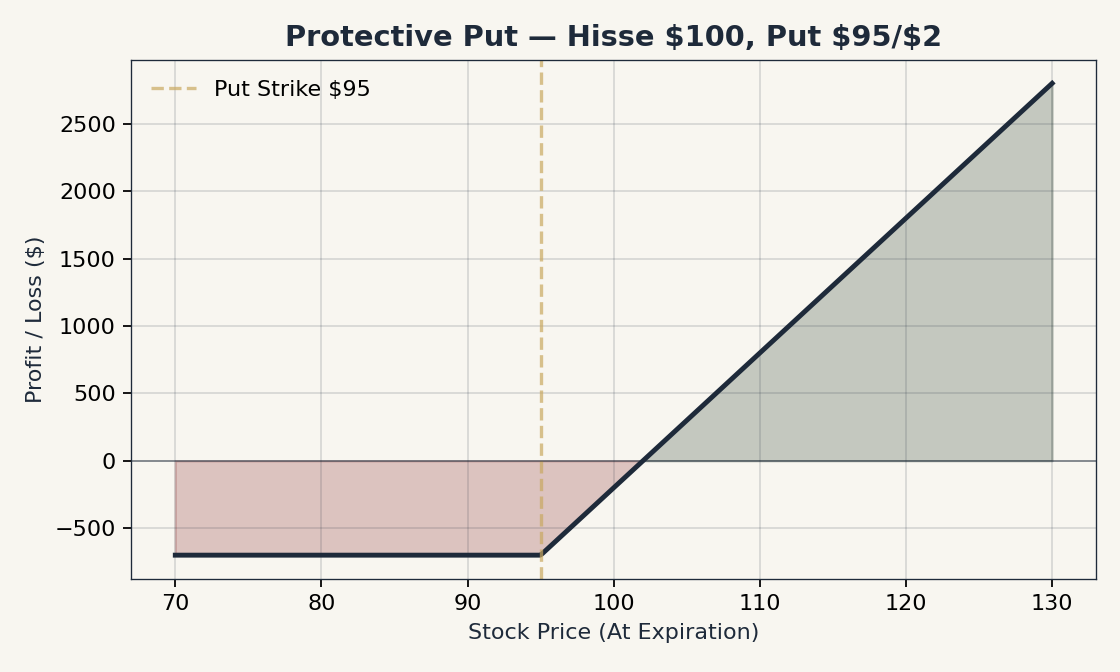

Protective Put — Insurance on One Position

Mechanic

-

Own 100 shares of stock (per contract).

-

Buy an OTM put against the position.

-

If the stock falls, the put gains value, offsetting the loss.

-

If the stock rises, the put loses (decays), reducing the gain.

Cost

The annual cost of protective puts varies with IV regime and strike distance:

-

5-10% OTM, rolling 30-60 day puts: roughly 4-8% of position value per year (in a typical IV environment).

-

Further OTM (say, 15-20% OTM): roughly 1-3% per year.

-

The cost can be twice as high in elevated IV regimes (post-crisis); half as much in extreme low-IV regimes.

This is a real drag on returns. A 3% annual hedging cost compounded over 30 years is significant. Whether it is worthwhile depends on whether you would otherwise sell through a drawdown — those who would not sell pay nothing for the hedge and miss its benefit; those who would sell may save themselves much more than the cost.

|

Protective puts are not for "always." They are tools for specific contexts:

Buying puts on every position, every month, perpetually, is a recipe for slow capital erosion in the typical bull-market regime. |

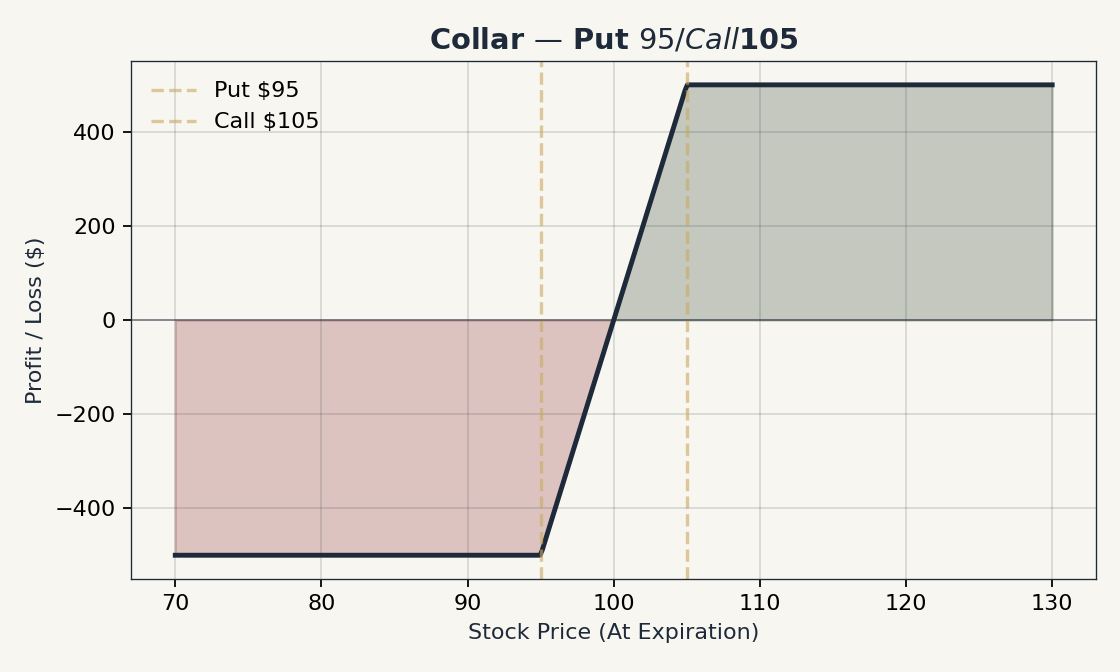

Collar — Insurance, Funded by Capping the Upside

Mechanic

-

Own 100 shares.

-

Buy an OTM put (protective leg).

-

Sell an OTM call (financing leg, like a covered call).

-

The premium received on the call offsets the put cost — sometimes fully ("zero-cost collar").

-

You have capped both the upside (above call strike) and the downside (below put strike).

Strike Selection

The classic "1-3 month, 5-10% OTM both legs" structure:

-

Long put at -5% OTM (delta around -0.20 to -0.30).

-

Short call at +5% OTM (delta around 0.20 to 0.30).

-

Net premium near zero, depending on skew.

The collar is the mainstream institutional hedging structure for concentrated single-stock positions (employee stock, founder equity). It is also used in retirement portfolios for "downside-guaranteed" stretches.

Trade-off

You give up the right tail of stock returns. If the stock rallies 30% above your call strike, you participate in only the first 5%. In a year with one extraordinary winner, this hurts.

But you have also bounded the left tail. A 30% crash takes you to the put strike, no further.

The choice is one of risk profile preference, not of return maximization. In expectation, the unhedged stock outperforms the collared stock over long periods (this is, after all, how the dealers make money). The collar buyer pays for psychological tolerance.

Choosing Between Protective Put and Collar

| Situation | Protective Put | Collar |

|---|---|---|

You expect significant upside |

Better (no upside cap) |

Worse (cap) |

You expect modest movement, fearful of downside |

Worse (premium cost) |

Better (cheap insurance) |

You want zero cost |

Not possible |

Often zero-cost |

You hold concentrated single-stock |

Useful |

Often preferred (institutional standard) |

You want to maintain flexibility |

More flexible (no upside obligation) |

Less flexible |

Management

-

Time decay on the put: as the put decays, you may need to roll it forward to maintain coverage.

-

Stock rises into the call: traditional collar approach — let the call assign; you sold at a price you were comfortable with.

-

Stock falls into the put: monetize the put (close at a gain) and re-set the structure with a new put.

-

IV spike during a drawdown: the put value can rise faster than expected (vega), giving an attractive exit opportunity.