Part III — Core Hunting Techniques · 7 min read

Vertical Spreads — Walking on Two Legs

"Welcome to the risk-defined world. Here the worst possible outcome is _known before you walk in."_

Four Verticals

Vertical spreads are the workhorse of the retail options market. A vertical is two options of the same type (both calls or both puts), same expiration, different strikes. There are exactly four possible verticals:

| Strategy | Direction | Net Flow | Expectation |

|---|---|---|---|

Bull Call Spread |

Up |

Debit (pay) |

Controlled up move |

Bear Put Spread |

Down |

Debit (pay) |

Controlled down move |

Bull Put Spread |

Up |

Credit (receive) |

Up or sideways |

Bear Call Spread |

Down |

Credit (receive) |

Down or sideways |

Each has its place. The key insight: spreads convert the three-bets-at-once problem of long options (direction, magnitude, timing) into something more manageable.

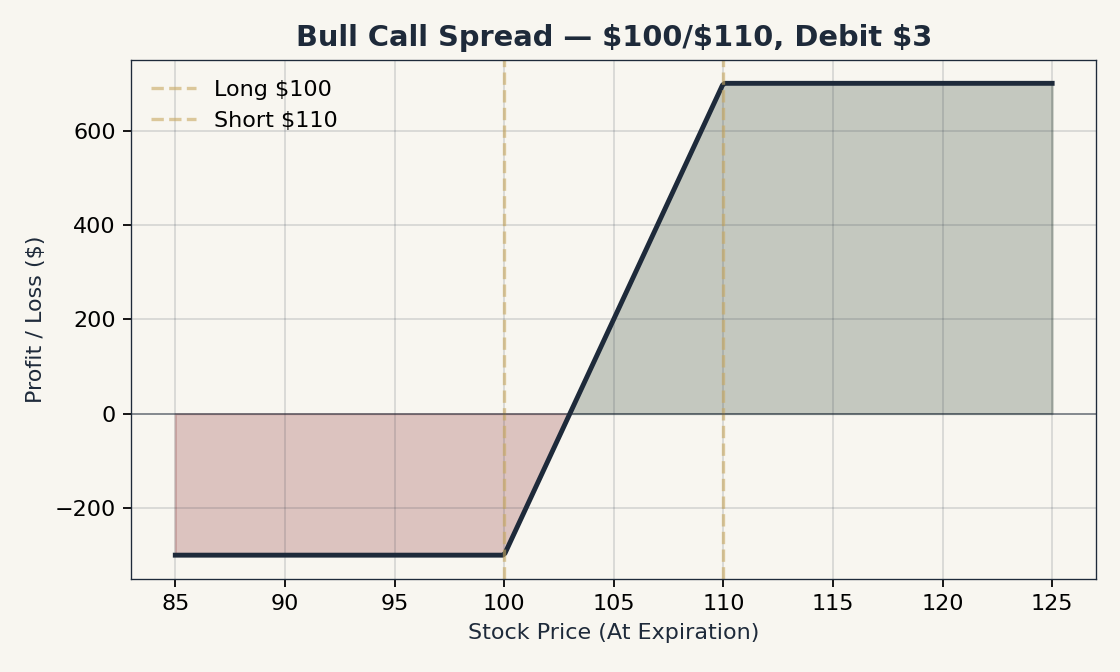

Bull Call Spread (Debit)

-

Buy a lower-strike call, sell a higher-strike call (same expiry).

-

Pay a net debit.

-

Maximum profit: spread width − debit paid.

-

Maximum loss: debit paid.

-

Break-even at expiry: lower strike + debit.

Example

AAPL is $175. You buy the $170 call for $7.00, sell the $180 call for $2.50. Net debit: $4.50. Spread width: $10.

-

Max profit: $10 − $4.50 = $5.50 per share, $550 per contract.

-

Max loss: $4.50 × 100 = $450 per contract.

-

Break-even: $174.50.

You have spent $450 for a position that pays up to $550 if AAPL rises to or above $180 by expiry. Compare that to buying just the $170 call outright at $700 — same upside scenario, but the call costs $250 more. The spread caps the upside but cuts the cost.

Bear Put Spread (Debit)

Symmetric to bull call. Buy a higher-strike put, sell a lower-strike put.

-

Net debit.

-

Max profit: spread width − debit.

-

Max loss: debit.

-

Break-even: higher strike − debit.

Bull Put Spread (Credit)

-

Sell a higher-strike put, buy a lower-strike put (same expiry).

-

Receive a net credit.

-

Max profit: credit received (if both legs expire OTM).

-

Max loss: spread width − credit.

-

Break-even at expiry: higher strike − credit.

Example

SPY is $450. You sell the $445 put for $3.00, buy the $440 put for $1.50. Net credit: $1.50. Spread width: $5.

-

Max profit: $1.50 × 100 = $150 per contract.

-

Max loss: ($5 − $1.50) × 100 = $350 per contract.

-

Break-even: $443.50.

The risk:reward is 350:150, or roughly 2.3:1. This sounds bad. But the probability of SPY ending above $443.50 in 30 days might be 70%. The expected value is:

-

0.70 × $150 + 0.30 × (−$350) ≈ −$0.

Roughly break-even in this example. Real edge in credit spreads comes from selling at higher delta strikes (better risk:reward) or capturing IV mean-reversion (selling at elevated IV).

Bear Call Spread (Credit)

Symmetric to bull put. Sell a lower-strike call, buy a higher-strike call.

-

Net credit.

-

Max profit: credit.

-

Max loss: spread width − credit.

-

Break-even: lower strike + credit.

When Debit vs Credit?

| Factor | Debit Spread (preferred when…) | Credit Spread (preferred when…) |

|---|---|---|

IV environment |

Low (you want IV expansion) |

High (you want IV contraction) |

Theta |

Slightly against you |

In your favor (collected on short leg) |

Probability of profit |

30-45% typical |

60-75% typical |

Risk:reward |

Better (1:1 to 1:3 favorable) |

Worse (3:1 to 5:1 unfavorable) |

Capital required |

Premium paid |

Collateral (often = max loss) |

A common phrasing: debit spreads are about big winners, credit spreads are about frequent winners. Both can work. Both can fail. Which one to use depends on the IV regime, your archetype (Chapter 7), and your view.

The Long Wing — Why It Matters

The "long leg" in a credit spread is not just margin relief — it is the cap on catastrophe. Without the long leg, you have a naked short option, and you have entered the unlimited-loss world of Chapter 5.

With the long leg, your loss is bounded. Always. This is why I will recommend, throughout this book, that beginning options traders default to spreads, not naked positions. The cost of the long wing — a couple dollars of premium given back — is the cost of buying yourself a maximum loss number you can stomach.

Management

-

Profit target (credit spread): Close at 50% of max profit. Why? The remaining 50% of profit comes with rising gamma risk in the final days.

-

Profit target (debit spread): Close at 50-80% of max profit, or at a specific delta target if you scale.

-

Loss management: A common rule is to close at 200% of credit received (you lose twice your max credit). Or — preferred — set a max loss in dollars equal to the max loss number on the spread, and accept that risk fully.

-

21-DTE rule applies to short side of credit spreads (Chapter 10).

Common Mistakes

-

Selling spreads too close to the money: high premium, low PoP, expected value often negative.

-

Sizing on credit, not max loss: "I collected $150 on this spread" is irrelevant. Size based on $380 max loss.

-

Treating an iron condor as two unrelated verticals: an iron condor is one position; do not "manage" one leg without considering the other.

-

Letting losers ride: a vertical that has gone fully ITM is a defined loss — close it, redeploy.

Multi-Leg vs Single-Leg

Some brokers charge per-leg commissions. A 4-leg iron condor (Chapter 16) at $0.65/leg is $2.60 to open and $2.60 to close — $5.20 round-trip vs $1.30 for a single call. On smaller premium trades, this commission load can erase the edge.

Choose brokers that quote spreads at a net price and execute them as a single transaction. Most discount brokers do; older firms may not.

Closing of Part III

Part III is done. You now know the four basic strategies:

-

Long Call & Long Put — direction bets with theta as the enemy.

-

Covered Call & CSP — income strategies with downside stock risk.

-

Protective Put & Collar — armor with a measurable cost.

-

Vertical Spreads — the risk-defined workhorse.

Master these four families and you have 80% of what the retail options market uses on any given day. Part IV will introduce more sophisticated structures, but the foundation here is sufficient for a lifetime of trading.