Part III — Core Hunting Techniques · 16 min read

Long Call and Long Put — The First Hunt

"A young wolf’s first hunt is almost always a rabbit — small, fast, and usually away. Fine. The first hunt teaches; it does not feed."

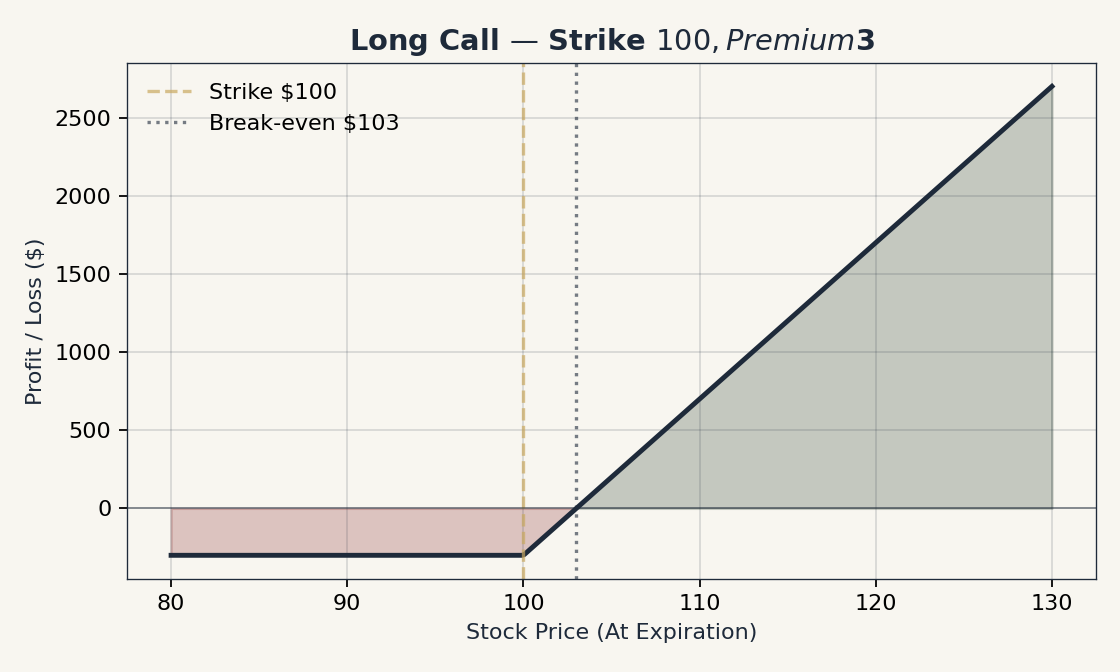

Long Call — The Bet Up

-

When: You believe the underlying will move substantially up within your timeframe.

-

Greeks: Delta + (your friend), Theta − (your enemy), Vega + (your friend if IV rises), Gamma + (your friend on big moves).

-

Max loss: Premium paid.

-

Max profit: Theoretically unlimited.

-

Break-even at expiry: Strike + Premium paid.

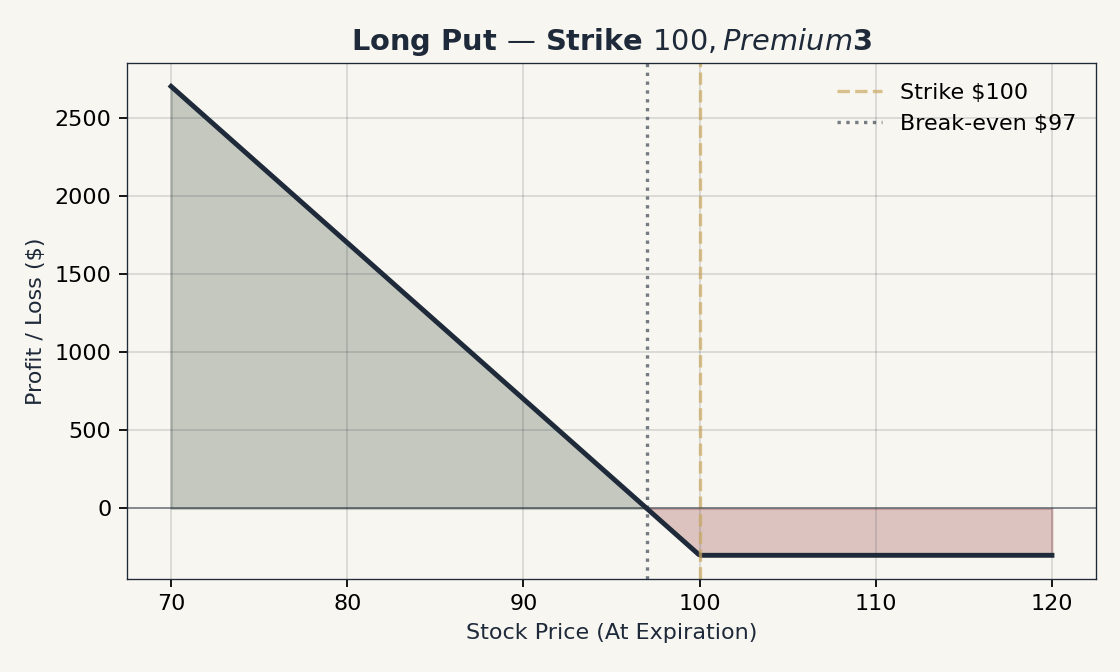

Long Put — The Bet Down

-

When: You believe the underlying will move substantially down within your timeframe.

-

Greeks: Delta − (your friend), Theta − (your enemy), Vega + (your friend if IV rises), Gamma + (your friend on big moves).

-

Max loss: Premium paid.

-

Max profit: (Strike − 0) × 100 − premium.

-

Break-even at expiry: Strike − Premium paid.

|

The "break-even at expiry" line is a textbook figure, not your management target. It tells you the price at which a position held all the way to expiration would zero out. The vast majority of real-world option trades never get there — they are closed early, on a premium-percentage move, long before expiration. The mindset for managing an option is not "did the stock cross my break-even line?" but "is the option’s premium up enough to take?" The "Hit-and-Run" section below makes this concrete. For now, treat break-even as a reference, not a goal. |

The Three Things You Must Be Right About

Buying a long option is not the same as betting on direction. It is betting on three things at once. Get any one wrong, and you lose.

-

Direction — does the stock move the right way?

-

Magnitude — does it move enough to overcome the premium plus extrinsic decay?

-

Timing — does it move within the option’s life?

Three different bets, all settled in the same trade. This is why most retail long-option positions on short-dated OTM contracts expire worthless — the trader rarely gets all three right (Sinclair, 2010, Ch 6).

The professional alternative: trade spreads (Chapter 14). A vertical spread converts these three independent bets into a more bounded single bet, at the cost of capping the upside.

Strike Selection — The Actual Skill

| Strike Region | Cost | Character |

|---|---|---|

Deep ITM (delta 0.80-0.95) |

High (intrinsic + small extrinsic) |

Behaves like the stock. Low leverage. High win rate. Vega exposure low. |

ATM (delta 0.50) |

Medium |

Needs direction and magnitude. Highest gamma & theta sensitivity. |

OTM (delta 0.20-0.35) |

Low |

Lottery-ticket character. Needs direction + magnitude + time. Vega exposure high. |

Deep OTM (delta < 0.10) |

Very low |

~95% expire worthless. Use only with full awareness of expectation. |

The Leverage Math (and Its Dark Side)

This is the section where I will show you why options are seductive — and dangerous.

Compare two positions, same direction, same dollar outlay. The underlying is AAPL at $175.

Position A: Stock

-

Buy 6 shares of AAPL at $175.

-

Capital outlay: $1,050.

Position B: Long 30-DTE ATM Call

-

Buy 1 AAPL $175 call at $3.50 premium.

-

Capital outlay: $350. (Use the remaining $700 in cash.)

Now compare what happens under three move scenarios over the next 14 days:

| Stock Move | Position A (6 shares) | Position B (1 long call) |

|---|---|---|

+5% (AAPL → $184) |

+$54 (5.1% on outlay) |

Premium ~$10, +$650 (186% on outlay) |

0% (AAPL stays $175) |

$0 |

Premium ~$2.10, −$140 (−40% on outlay, theta) |

−5% (AAPL → $166) |

−$54 (−5.1% on outlay) |

Premium ~$0.40, −$310 (−89% on outlay) |

The upside asymmetry is breathtaking: a 5% stock move becomes a 186% return on the option. This is the leverage that draws traders into options.

The downside asymmetry is harsher: a flat market — not even adverse — loses 40% on the option. A 5% adverse move nearly wipes out the position.

This is the leverage trade-off:

-

In return, you give up your "right to be patient." A stock can stay flat for weeks and you are unharmed. An option cannot.

-

In return, you give up your "right to be wrong about timing." A stock move that takes three months works for stockholders. The same move loses for a 30-day option holder.

|

The leverage of long options is not free. It costs theta every day and vega on every IV change. The seduction is the upside multiplier. The danger is that you pay the leverage premium every single day — even on days when nothing happens. |

The Spot Price Effect — Detailed View

Suppose AAPL is at $175 on a Tuesday morning. You hold three different calls:

| Strike | Delta (start) | If AAPL → $180 (+$5) | If AAPL → $185 (+$10) |

|---|---|---|---|

$170 (ITM) |

0.72 |

Premium ~+$3.80, gamma adds a touch |

Premium ~+$8.40, near parity with $10 |

$175 (ATM) |

0.50 |

Premium ~+$2.80 (delta + gamma) |

Premium ~+$6.70 (gamma was big) |

$180 (OTM) |

0.30 |

Premium ~+$1.80 (gamma helped, now ATM-ish) |

Premium ~+$4.50 |

Two observations:

-

Gamma is most rewarding on ATM moves. The ATM call’s premium roughly doubles on a $10 move, because gamma kept ratcheting delta upward.

-

Deep ITM calls track the stock almost dollar-for-dollar. They give up leverage in exchange for behaving like the stock. This is the foundation of LEAPS-as-stock-replacement, covered in Chapter 19.

A practical takeaway: if you have a strong directional view and want close-to-stock behavior with capped downside, buy ITM (delta 0.70+). If you want leverage and accept the higher loss probability, buy ATM or moderately OTM. If you want a lottery ticket, OTM with full awareness.

Theta Deep Dive

Long options bleed time. Here is the bleed in detail.

| DTE Range | Theta Behavior | What You Feel |

|---|---|---|

90 → 60 |

Slow drip |

~0.1-0.3% of premium per day |

60 → 30 |

Modest decay |

~0.3-0.7% of premium per day |

30 → 14 |

Acceleration begins |

~0.7-1.5% of premium per day |

14 → 7 |

The cliff |

~2-5% of premium per day |

7 → 0 |

The avalanche |

~5-15% of premium per day; final 48 hours nearly all extrinsic |

For an ATM 30-DTE option at $3.00 premium, theta is approximately $0.06 per day. That sounds small until you realize that is $6 per day per contract, every calendar day until expiry. On 5 contracts, $30 per day. In a week of no movement, you have lost $210 sitting still.

The non-linear acceleration is critical (Natenberg, 2014, Ch 7). A 30-DTE option does not lose 1/30th of its time value each day. It loses much less in the first 15 days and much more in the last 15. By DTE-7, theta dominates everything else.

The Practical Implication

-

For long options: do not buy short DTE unless you want maximum leverage and accept the theta avalanche. The "sweet spot" for buyers is 30-45 DTE, where theta is manageable.

-

The day-by-day premium decay graph is steepest under 30 DTE. If you find yourself "waiting" for direction past day 15 of a 30-DTE contract, you are paying acceleration costs.

-

For short-premium sellers, the inverse: theta is income, and the 21-45 DTE window is the harvest zone.

Weekend Theta — The Three Days You Pay For One

Options price time in calendar days, not trading days. A Friday-close to Monday-open window is roughly three calendar days of theta — but only one day of opportunity to react to anything.

Market makers know this. They do not wait for Monday to take the decay; they front-load the weekend theta into the Friday afternoon premium. Practical observations:

-

Friday afternoon on a long-premium position: visible accelerated decay. Premium that was $2.10 at noon Friday can be $1.85 by close — a meaningful chunk of the three-day weekend already priced.

-

Monday open: relatively flat theta. Market makers have already "collected" the weekend decay; new theta from Monday onward begins fresh.

-

Net effect over Friday-to-Monday: about three days of decay, distributed unevenly with most of it crystallized on Friday.

For long-premium holders this is a structural headwind: a position carried from Friday into Monday pays three days of theta in exchange for zero trading days. For short-premium sellers it is the same effect in reverse — you collect three days of theta over a 65.5-hour window, but you cannot adjust if news hits over the weekend (cf. Chapter 9 "Gap Risk"). The cost of the weekend is real, and the gap risk over the weekend is real. Both ledger entries belong on the same page.

Long premium going into a Friday close:

-

If your directional thesis is not playing out by Friday afternoon, closing before the bell often beats holding through the weekend — you save the three-day theta and avoid the gap.

-

If your thesis is playing out, the weekend is a binary risk: news in your favor doubles the gain; news against you erases the position. Size accordingly.

Short premium going into a Friday close:

-

The weekend theta is genuinely attractive — three days of decay, single seller premium.

-

The catch: you cannot hedge over the weekend. If a counterparty’s bad news hits Saturday morning, your position is "locked" until Monday.

-

For naked short premium, going into a weekend with a binary catalyst is essentially uninsured speculation. Defined-risk structures are far more weekend-tolerant.

Hit-and-Run vs Hold to Expiry

A question every new trader asks: should I close my long option early, or hold it to expiration?

The short answer: almost never hold to expiration. The way real-world option traders use options is hit-and-run. You buy the option, the premium moves, you exit at a percentage gain (or cut at a percentage loss). The stock-price target — the textbook break-even — is rarely the framework that actually fires the exit. The framework is the option’s premium.

A long call bought at $2.00 might be closed at $3.00 (+50%), $4.00 (+100%), or $6.00 (+200%) — regardless of where the stock is. The exit rule is a number on the option’s premium, not a number on the stock chart. This is how most retail and most professional directional-options traders actually operate; it is also how the books that teach "wait for the stock to hit your strike + premium" lead beginners astray. You manage the option, not the stock.

Two practical reasons this matters:

-

Options decay every day. Even if the stock eventually reaches your textbook break-even, theta may have eaten so much premium that you make less than expected — or nothing.

-

The biggest profit on a long option often happens early. Gamma magnifies the first sharp move. If you wait for "more," you frequently watch it give back.

Position sizing is the second half of this. Because options are leveraged (Chapter 6 on sizing; the leverage math earlier in this chapter), a +100% move on the option might be only a 5-8% move on the stock — but it is a 100% move on your premium, and you should treat that as the meaningful number for both profit-taking and risk control. A trade sized too large means a single bad +100% loss erases many small wins. A trade sized correctly means many +50% wins compound.

The Industry Data

The OCC’s clearing statistics show that the majority of US-listed options are closed before expiration — not held. Estimates vary, but published OCC and exchange data have consistently shown:

-

Approximately 60-70% of options positions are closed before expiration.

-

Approximately 10-20% are exercised (most of these are deep ITM at expiry).

-

Approximately 20-30% expire worthless.

(See OCC operational reports; specific percentages vary year to year.)

Most positions are closed early. The "hold to expiration" approach is the minority.

Why Most Traders Close Early

-

Gamma risk explodes in the last 7-10 days. Holding through this period means accepting whipsaw and pin risk.

-

Slippage on automatic exercise can be poor. If your call is $0.10 ITM at expiry, you may end up with shares at the strike when you wanted to capture the option premium.

-

Pin risk (Chapter 9) on short positions.

-

The remaining time value is small in the last week. The reward for holding is shrinking; the risk is growing.

When Holding Makes Sense

-

Deep ITM with no extrinsic value remaining. The option is effectively a stock proxy. Holding to expiry and exercising for shares can be cleaner than closing.

-

Defined-risk structures where automatic expiry produces a clean outcome. An iron condor where both sides finish OTM expires worthless and you keep the credit — no action needed.

-

European-style cash-settled options (SPX) where pin risk does not apply and settlement is automatic.

Practical Heuristics

These are conventions widely used in active options trading, especially by tastytrade-school practitioners (cite Sosnoff & associates; Sinclair, 2010 also discusses similar ranges):

| Position Type | Profit Target | Loss/Manage Trigger |

|---|---|---|

Long premium (calls, puts) |

+50-100% gain → take |

−50% loss → cut |

Short premium (CSP, CC, naked) |

25-50% of credit → take |

Manage at 21 DTE; 100-200% loss → cut |

Spreads (verticals, condors) |

50-80% of max profit → close |

100-200% of credit lost → cut |

The 21-DTE rule — a common convention in short-premium trading — recommends closing or rolling short positions when they have ~21 days to expiry, regardless of P&L. The reasoning: gamma risk steepens dramatically inside 21 DTE, and the remaining theta available to harvest is small. Better to roll into a new 45-DTE position than to ride gamma.

|

Most short premium plays should be closed at a profit target, not held to expiration. Holding for "the last 10%" frequently exposes you to gamma risk that destroys far more than the 10% you were trying to capture. This is why discipline beats hope. A consistent take-profit at +50% on long premium, applied across many trades, produces a smoother equity curve than a strategy of "letting winners run to expiration." |

Expiration Selection

Expiration choice for a long call or long put is a topic large enough to warrant its own chapter. The default recommendation for most retail long-premium trades is the 30-45 DTE window — meaningful theta exposure, manageable gamma, vega secondary.

For the full treatment of expiration regimes — 0DTE, weekly, the 30-45 DTE sweet spot, mid-dated, and LEAPS — including OPEX days, quad-witching, and the decision framework, see Chapter 11: Choosing Your Expiration.

Management — After the Trade is Open

-

In profit: take profit at +50-100% on long premium. Walk away.

-

In loss: take loss at −50% on long premium. Walk away.

-

Theta is eating: if DTE < 14 and the move has not yet happened, close. The remaining theta is not worth the wait.

-

Earnings approaches: be aware of IV crush. Roll out to post-earnings expiry, or close pre-event.

Common Mistakes (Young Wolves)

-

OTM lottery: cheap strike, short DTE, ~95% finish worthless.

-

Long premium into earnings: IV crush wipes out the trade even on right direction.

-

Wrong about "I’m sure": directional confidence does not solve the three-bets-at-once problem.

-

Ignoring theta: "I’ll wait for it to come back." It is not coming back. It is melting.

-

No stop: "premium goes to zero, what’s the worst that could happen?" The worst is doing this fifty times.