Part IV — Advanced Two-Legged Hunting · 6 min read

Iron Condor and Iron Butterfly — Hunting the Sideways

"The most efficient hunt is the one where nothing has to happen."

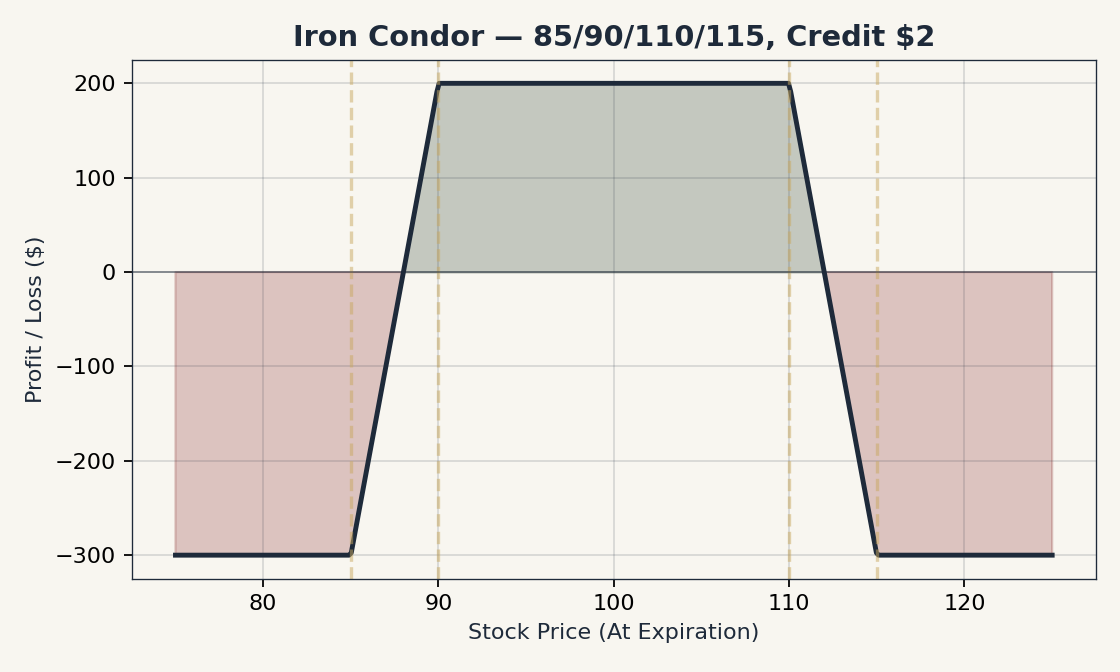

Iron Condor — Four Legs, Two Wings

Mechanic

-

Bull put spread (below the current price): sell a put, buy a further-OTM put for protection.

-

Bear call spread (above the current price): sell a call, buy a further-OTM call for protection.

-

All four legs same expiration.

-

Net credit (sum of both spread credits).

The structure is delta-neutral at inception if symmetric. You profit if the underlying stays inside the two short strikes by expiration. You lose if the underlying breaks through either short strike.

Payoff

The shape is a plateau bounded by two cliffs. Inside the wings: full credit. Outside: defined loss.

Strike Selection

-

Inner short strikes (the puts you sell + the calls you sell): typically delta 0.15-0.20 each. Together, you have a ~70% probability of the underlying ending inside both shorts.

-

Outer long strikes: 5-10 points wider than the shorts. The wing width determines max loss.

-

Symmetric around current price for delta-neutral; asymmetric if you have a directional bias.

Example

SPX is at 4500.

-

Sell 4400 put, buy 4390 put. Put spread credit: $1.00.

-

Sell 4600 call, buy 4610 call. Call spread credit: $1.00.

-

Total net credit: $2.00 → $200 per contract.

-

Wing width: 10 points.

-

Max loss per spread: ($10 − $1) × 100 = $900. Per side. But only one side can lose at expiry.

Maximum profit: $200. Maximum loss: $900 − $100 (the credit on the other spread that expires worthless) = $800. Risk:reward of 4:1 against you. The trade is sized for high PoP, not high payoff.

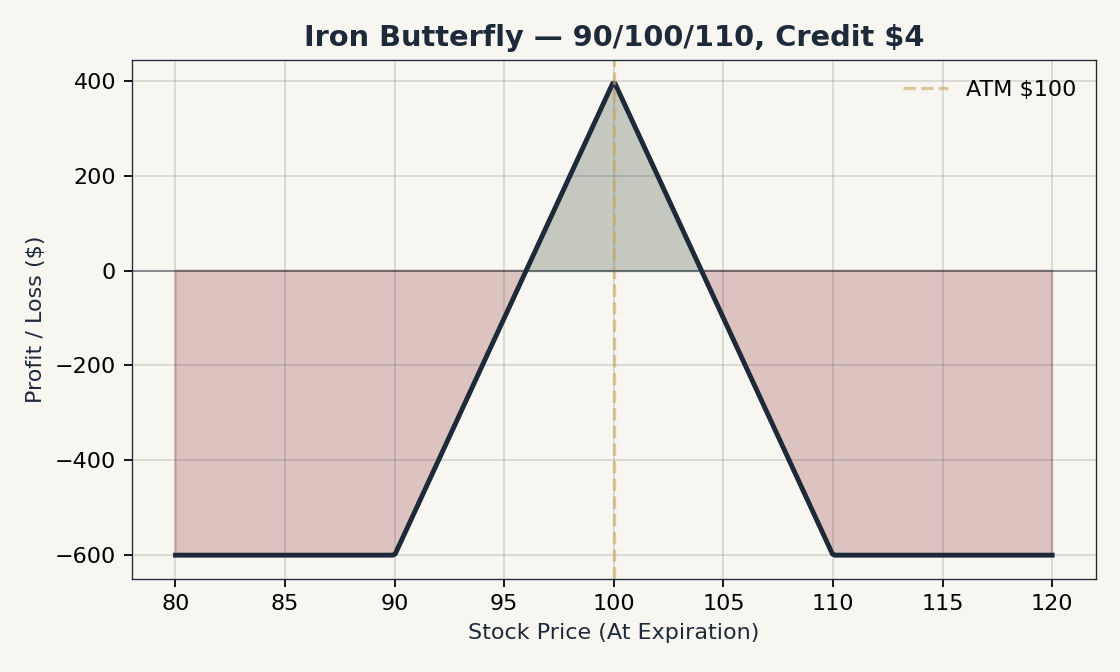

Iron Butterfly — Tighter, Richer

Mechanic

A variant of the iron condor where the short put and short call are at the same strike — i.e., ATM. The structure becomes:

-

Short ATM put + Short ATM call (a short straddle, in fact).

-

Long OTM put + Long OTM call (the wings).

Payoff

A tighter peak at ATM, sharper drop-offs. Compared to a condor:

-

Credit collected: roughly 3-5× higher (because you sold ATM premium).

-

Profit zone: much narrower.

-

Maximum profit point: exactly at the short strike at expiry.

When to Choose

| Use Case | Iron Condor | Iron Butterfly |

|---|---|---|

Mild range expectation |

Better |

Less ideal |

Strong conviction underlying will park at one strike |

Less ideal |

Better |

Want wider PoP, accept smaller credit |

Better |

Worse |

Want larger credit, accept narrower PoP |

Worse |

Better |

Hedging an existing directional position |

Often |

Rare |

Greeks Profile

| Greek | Iron Condor at Inception |

|---|---|

Delta |

~0 (neutral if symmetric) |

Theta |

+ (your friend, premium decays) |

Vega |

− (IV contraction helps; expansion hurts) |

Gamma |

− (negative gamma intensifies near expiry) |

The negative-gamma exposure is critical. As expiration approaches, gamma on the short strikes becomes large. A small move in the underlying can transform the position from "profitable" to "max loss" quickly.

Management

-

25-50% profit: take. Conventional wisdom in short-premium trading: a $200 credit that has decayed to $100 is "halfway there" — close, do not push for the last 50%. The remaining profit comes with rising gamma risk.

-

One wing breached: close the threatened side or close the whole structure. Rolling the unbreached side closer to the money to collect more credit is a common adjustment, but it adds risk and is contested in the literature (some practitioners avoid it altogether — see e.g. discussions in Sosnoff’s market-making framework, tastytrade).

-

21 DTE: convention applies. Close or roll regardless of P&L.

-

Vol expansion: a rising VIX or sector vol can hurt the condor through vega; manage if vega losses approach your max loss.

Common Mistakes

-

Selling condors during high-event windows: earnings, FOMC, CPI — these are not "range" environments.

-

Letting them go to expiry: gamma risk is brutal in the last week.

-

Treating wings as decoration: the wings are the only thing limiting your loss. Do not let them slide too far OTM thinking "the underlying will never get there."

-

Selling too close to ATM for "more premium": PoP collapses quickly; the higher credit reflects the lower probability.