🧬 What is GEX (Gamma Exposure)?

Gamma Exposure (GEX) turns options open interest into a positioning map — a way to see where dealer hedging flows are likely to concentrate, and whether those flows tend to calm a market down or speed it up. This page builds the idea from the ground up: what gamma is, who hedges it, and how positive and negative gamma regimes shape the volatility and price behavior traders watch every day.

Gamma — The Short Version#

Every options contract has a gamma value. Gamma measures how fast an option's delta changes when the underlying stock moves $1. Higher gamma means the option's sensitivity to price changes is accelerating.

Who Cares About Gamma? — Dealers Do#

When you buy a call option, a market maker (dealer) sells it to you. They're now short gamma. To stay hedged, they must buy shares as the stock goes up and sell shares as it goes down. This is called delta hedging.

The more open interest at a strike price, the more shares dealers need to trade for hedging. This creates measurable buying and selling pressure at specific price levels.

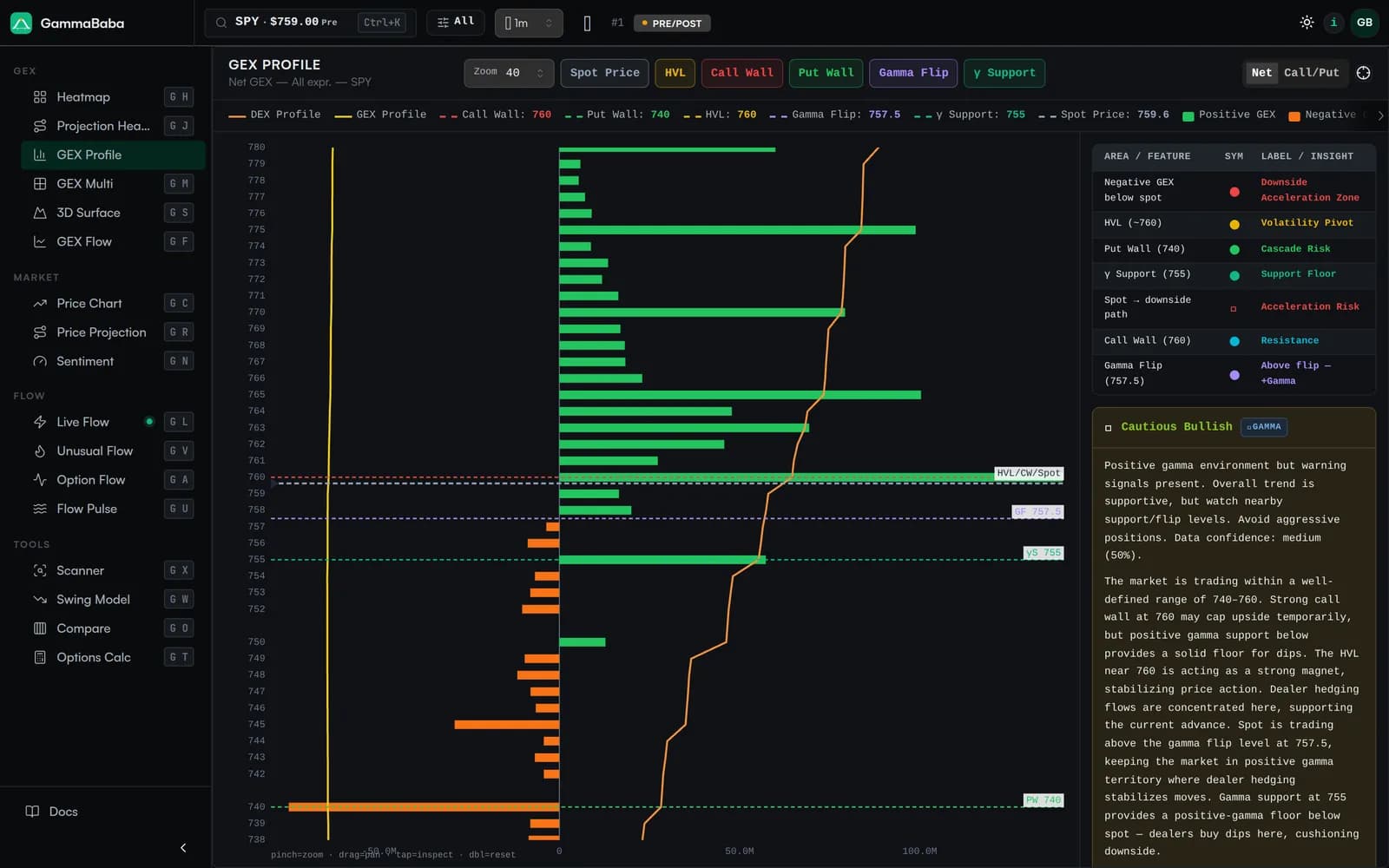

How GEX is Measured#

Gamma Exposure (GEX) estimates the dollar size of the hedging flow that the assumed short-gamma side must execute for a given move in the underlying. Our in-house gamma engine evaluates this per contract and then aggregates it by strike and expiration, weighing each contract by how concentrated positioning is and which side of the trade is assumed to be short gamma.

- Each contract's per-unit gamma is treated as a non-negative value for both calls and puts. The sign of GEX comes from the convention applied to the contract type, not from gamma itself.

- Open interest at each strike and expiry scales the magnitude, and the standard contract multiplier (shares per contract) translates positioning into share-equivalent hedging size.

- Calls contribute positive GEX and puts contribute negative GEX — this is the convention used across the platform. It assumes the common "dealer short calls / dealer short puts" framing; real positioning can differ on any given day.

Two scaling modes are available:

- Per $1 move (default) — the hedging size implied by a one-dollar move in the underlying.

- Per 1% move — normalized to a one-percent move instead, which makes the magnitude comparable across tickers with very different price levels (for example comparing a $500 ETF with a $20 stock).

Why GEX Matters#

Large GEX concentrations create mechanical hedging pressure that can influence price behavior:

- High positive GEX (blue) — Dealers are long gamma. They sell into rallies and buy dips → tends to dampen volatility, creating a zone where price often consolidates.

- High negative GEX (red) — Dealers are short gamma. They sell into dips and buy into rallies → tends to amplify volatility, creating conditions where moves can accelerate.

Positive vs Negative GEX Environment#

| Environment | Dealer Behavior | Typical Market Characteristic |

|---|---|---|

| Net Positive GEX | Buy dips, sell rips | 🧲 Lower vol, mean-reversion tendency, pinning |

| Net Negative GEX | Sell dips, buy rips | 🔥 Higher vol, trend acceleration, gaps |

On the heatmap, those regimes become visible at a glance. Strikes stacked with positive GEX form call walls that often cap rallies; strikes loaded with negative GEX form put walls that can act as a floor. The strike carrying the heaviest gamma — the King Strike — frequently lines up with where price gravitates as expiration approaches.

Where the Data Comes From#

GammaBaba consumes real-time options snapshots — strike prices, open interest, volume, last prices, and greeks when available. When a contract's greeks aren't reported, gamma is estimated from the contract's own market-implied volatility using a proprietary GammaBaba options-pricing model, so each strike and expiration gets its own IV — no single flat volatility is assumed across the board.

Spot prices and market data refresh continuously during US market hours.